- The Range

- Posts

- For the Market's Next Trick...

For the Market's Next Trick...

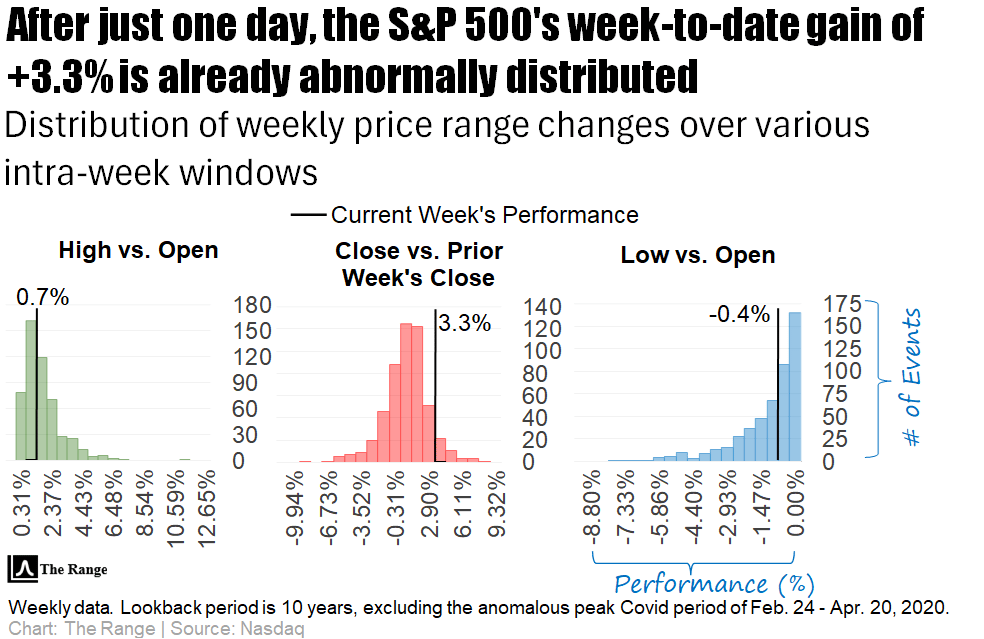

Hello and welcome! 👋 While yesterday’s 3.3% rally (the largest 1-day rally since April 9th and the 2nd largest since November 2022) was firecracker of a move for the S&P 500, it was kind of a snooze-fest on the economic front. But don’t get too comfy—things are about to heat up with the release of April’s Consumer Price Index (CPI).

Last month’s surprise dip in inflation had everyone breathing a little easier. According to economists, however, investors shouldn’t expect a repeat. Economists are bracing for signs that those February tariffs are finally starting to hit the data.

For now, forecasters expect CPI to tick up 0.3% month-over-month and 2.3% year-over-year. Core inflation (a.k.a. everything minus your grocery runs and gas station pit stops) is also expected to rise 0.3% on the month and 2.8% annually.

And while earnings season is winding down, a few names are still on deck—keep an eye on JD.com, Under Armour, Intuitive Machines, Oklo, and Petrobras. Not a blockbuster lineup, but enough to keep things interesting.

Remember, on Tuesdays and Thursdays we deliver abridged emails. We’ll be back in full swing for Wednesday’s newsletter.👊👊

Clearly, with the S&P 500 rallying more than its 2 standard deviation implied move on Monday, market makers were not anticipating that a noteworthy trade deal to be hammered out over the weekend. Prior to Monday’s rare rally, the S&P 500 had closed within its implied daily range during 9 of the prior 10 trading sessions.

With the details of this weekend’s temporary trade agreement now priced in, the market is expecting the S&P 500 to trade between 5788 and 5900 on Tuesday.

Please be sure to follow us on X.

If you like what we're doing, please forward us to a friend. If you're not already subscribed, join our growing family of free subscribers.

Reply