- The Range

- Posts

- Big Stakes Ahead: Tariffs, Tech Earnings, the Fed, and Seasonal Headwinds Take Center Stage

Big Stakes Ahead: Tariffs, Tech Earnings, the Fed, and Seasonal Headwinds Take Center Stage

Trade Truce Boosts Global Markets Ahead of Pivotal Central Bank Week

👋Hello and Happy Monday! 🌅

Here’s what’s on deck this week:

📆 Big week incoming: A fresh round of Fed drama and a key tariffs deadline are set to steal the spotlight on Wall Street.

💰 Earnings-palooza: Tech titans Microsoft, Meta, Apple, and Amazon are all reporting this week—so yeah, it's kind of a big deal.

📊 Data drop: July’s jobs report and the latest inflation figures are on deck, giving investors more tea to sip on the state of the economy.

📈Markets rally, but watch out for August headwinds: Global markets are rallying after fears of an all-out trade war with the EU have eased, but don’t sleep on bearish August seasonality.

Let’s dive in.💦💦

Be sure to follow us on X, where we update our comprehensive daily performance charts and other timely intra-week statistics daily.

Click here 👈to learn more about our charts.

The countdown to August is heating up on the trade front. President Trump’s Aug. 1 tariff deadline is looming, and unless the U.S. locks in more deals with some of its biggest trading partners—including Canada, and Mexico—those countries could be staring down tariffs of 30% or more. Talks with China are also on the docket ahead of an Aug. 12 deadline, though that one’s widely expected to get kicked down the road.

Meanwhile, Trump is turning up the heat on the Fed as it prepares for its interest rate decision on Wednesday. Spoiler alert: Most expect the central bank to keep rates steady. But investors will still be glued to this week’s economic data, looking for clues on what comes next. Thursday’s personal consumption expenditures report will show whether inflation is still running hot, and Friday’s jobs report could add fuel to the “higher for longer” fire. The Fed’s made it clear: as long as the job market stays strong, don’t expect rate cuts anytime soon.

We’ll also get the first read on Q2 GDP. After a mild contraction in Q1, markets are eager to see whether the economy is back in the green—or still struggling to find its footing.

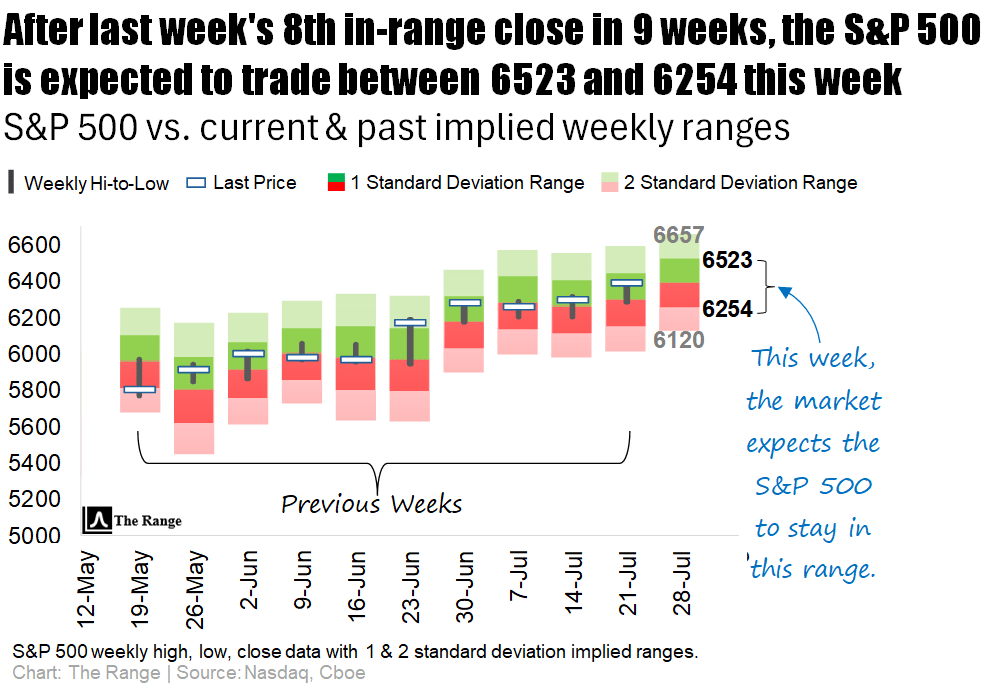

Despite all the big happenings this week, a look back at the past 20 years of strong S&P 500 uptrends suggests that there is an 80% chance the S&P cash index (SPX) will close within its implied 5-day range between 6254 and 6523.

Big Tech is stepping back into the spotlight this week, with more than half of the Magnificent Seven gearing up to report earnings—and they’re not alone. Heavy hitters across health care, crypto, finance, and autos are also lining up at the mic.

Meta kicks things off Wednesday, and Wall Street will be watching closely for updates on the company’s AI spending spree. Microsoft reports the same day, riding high on investor hype around its AI dominance. Then comes Apple on Thursday, where analysts are eager to see whether Cupertino is finally getting serious about catching up in the AI arms race. Amazon, fresh off a buzzy Prime Day, will round out the week’s Big Tech parade.

Outside the silicon crowd, Mastercard and Visa could offer a sneak peek at how consumers are swiping their way through summer. Procter & Gamble, Colgate-Palmolive, and Starbucks will drop clues about everyday demand and pricing power.

Over in the health care sector, earnings from UnitedHealth, AstraZeneca, Merck, AbbVie, and Bristol Myers Squibb could provide a broader check-up on the industry. And with Bitcoin back near its highs, Strategy and Coinbase step into the earnings spotlight Thursday. Lastly, Ford will give its update Wednesday as automakers continue to wrestle with tariff pressures.

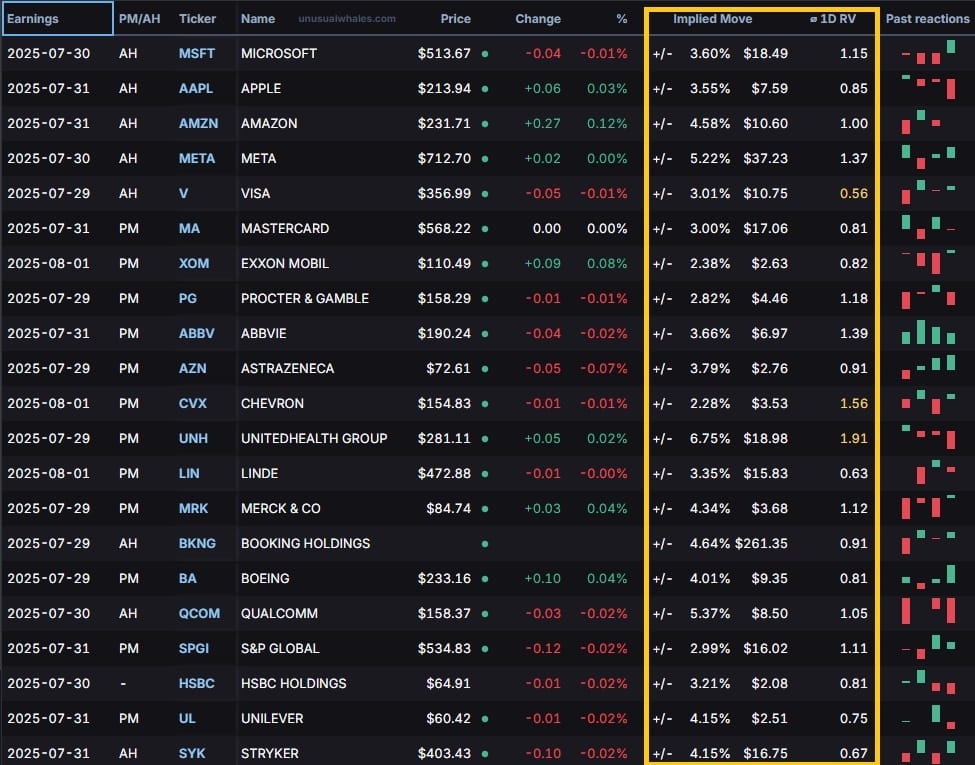

👇 Below, we’ve got a cheat sheet of this week’s biggest names reporting, sorted by market cap (source: Unusual Whales).

For active traders looking for actionable insights, the highlighted columns show the implied (expected) post-earnings move for each company, along with the Average 1-Day Realized Volatility Post Earnings Ratio (1D RV).

📈Implied Move: The market’s best guess at how much a stock will swing after earnings.

📊1D RV: A powerful tool that represents the post-earnings price move divided by the expected price move over the past 12 quarters. In other words, it measures how good (or bad) the market is at pricing each company’s earnings.

💵When you see a ratio >1.0, indicates that, historically, the earnings are mispriced and the stock moves MORE than the market anticipates, favoring straddle buyers.

🪝A ratio <1.0 tells the opposite story, meaning the stock historically moves LESS than the market anticipates, which favors straddle sellers.

Happy hunting.

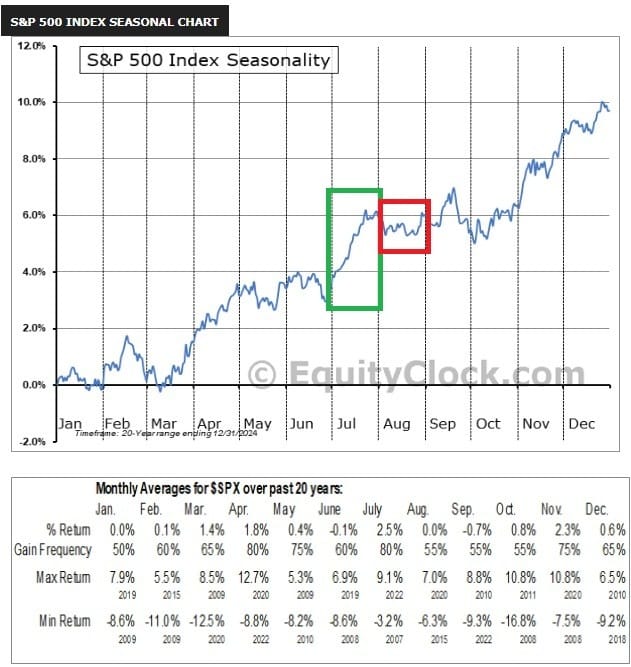

Seasonal Headwinds Are in the Forecast

After a red-hot July rally, the stock market might be flying a little too close to the sun. As this 20-year chart of the S&P 500’s average monthly performance from charts.equityclock.com shows, August (red square) hasn’t exactly been Wall Street’s favorite month after what is typically a strong July (green rectangle)—unless you’re a bear.

Over the past two decades, the S&P 500 has averaged a modest loss in August, making it one of the weakest months of the year. But just like the weather, forecasting seasonal trends is tricky. Seasonality can be helpful for planning—but it’s no guarantee. Momentum has been strong, especially in tech and energy. Still, if volatility starts to creep in (👀 VIX), don’t say history didn’t warn you.

So if you’re riding the July high, consider tightening your protective stops as we head into the final stretch of July.

🇪🇺 Trump deal with Europe underlines new standard of at least 15% tariffs: Trump’s latest tariff tango with Europe sets a new “15% or bust” vibe for global trade. The EU might fall in line or clap back with economic espresso shots of its own. Read more

🤝 US, China talk in Stockholm as trade tensions simmer: The U.S. and China met in Stockholm to sip some neutrality and avoid collapsing the global economy (again). No handshakes, no fireworks—just a diplomatic staring contest. Read more

⚡ Why Tesla’s valuation is hard to read as Musk’s EV empire falters: Tesla’s stock is wobbling like a self-driving car on a beta test route. Between EV slowdowns and market rivals, even investors aren’t sure if it’s brilliance or battery burnout. Read more

Gif by snl on Giphy

🛩️ Boeing's fighter jet workers in the St. Louis area reject contract, threaten strike: Boeing’s jet builders are gearing up to launch more than just aircraft—think picket signs and tense negotiations. If management doesn’t budge, things might get turbulent on the ground. Read more

🌽 What does 2025 corn crop pollination look like in July?: Midwest farmers are watching their crops like hawks, hoping July’s weather doesn’t turn their corn into popcorn. Pollination can make or break the crop—but Mother Nature’s schedule is more chaos than calendar. Read more

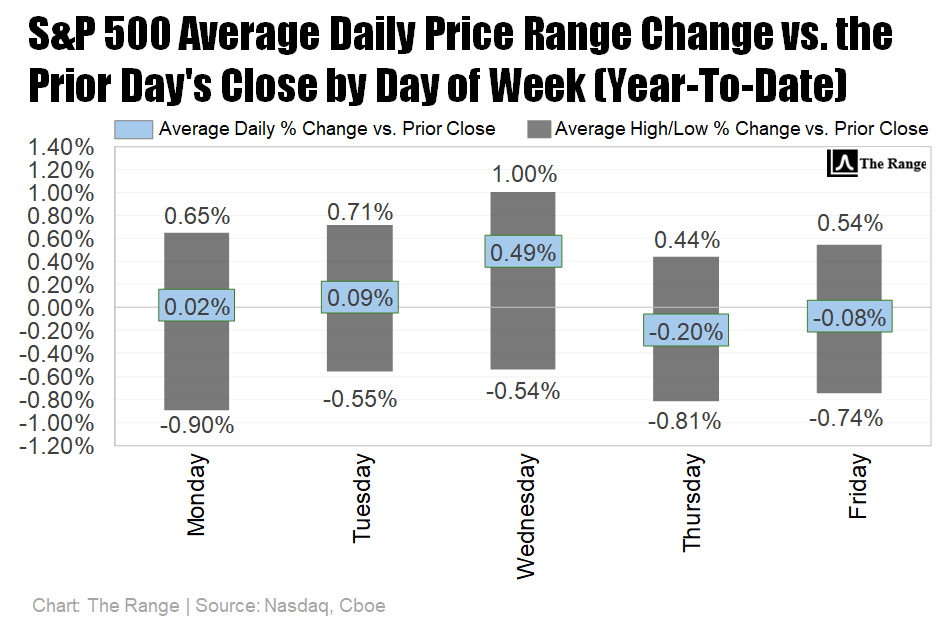

The CBOE Volatility Index (VIX) has now spent 11 straight weeks below 20, and last week’s close below 15 was the first since early February. Until we see a reversal of this trend, look for the S&P 500 to remain true to its typical daily and weekly price swings.

EDITOR’S NOTE

Each day the market is open, we update our comprehensive daily performance charts on our website for you to view. In addition, followers can find timely statistics on our X feed.

Monday

Key Earnings: Welltower, Waste Management, Cadence Design Systems

Tuesday

U.S. trade balance (June)

Key Earnings: Visa, Procter & Gamble, UnitedHealth Group, AstraZeneca, Merck, Booking Holdings, Boeing, Spotify Technology, Starbucks, Royal Caribbean Group, United Parcel Service

Data to Watch: Retail inventories (June), wholesale inventories (June), S&P Case-Shiller home price index (May), consumer confidence (July), job openings (June)

Wednesday

FOMC interest-rate decision

Fed Chair Jerome Powell press conference

Key Earnings: Microsoft, Meta Platforms, HSBC Holdings, Qualcomm, Arm Holdings, Robinhood Markets, Carvana, Allstate, Ford

More Data to Watch: ADP employment (July), gross domestic product (Q2), pending home sales (June)

Thursday

Personal consumption expenditures (PCE) (June)

Key Earnings: Apple, Amazon, Mastercard, AbbVie, Comcast, Ferrari, Strategy, Coinbase, Bristol Myers Squibb, CVS Health

More Data to Watch: Employment cost index (Q2), initial jobless claims (Week ending July 26), Chicago Business Barometer (July)

Friday

Tariff deadline for Canada, Mexico, the European Union, and other trading partners

U.S. employment report (July)

Key Earnings: ExxonMobil, Chevron, Colgate-Palmolive

More Data to Watch: Consumer sentiment - final (July), construction spending (June), ISM Manufacturing Purchasing Managers Index (July), S&P Manufacturing PMI (July)

Below is our curated list of top value-added insights that uncover what’s happening way beyond the usual financial media headlines.

Not a super great sign over the next couple of months, especially if we start to see a cluster of readings.

— Jason Goepfert (@jasongoepfert)

12:25 PM • Jul 27, 2025

Observation: The RSI is used to justify one's bias 📉📈

For instance, market bears have cited the indicator in two distinct ways the last few months:

1️⃣ $SPX hits new highs & RSI > 70 → “Overbought = bearish”

2️⃣ $SPX hits new highs & RSI < 70 → “Negative divergence =

— Frank Cappelleri (@FrankCappelleri)

4:14 PM • Jul 26, 2025

GS: Trade agreements with the US have been a market-clearing events for most equity markets

— Mike Zaccardi, CFA, CMT 🍖 (@MikeZaccardi)

10:12 PM • Jul 27, 2025

On a recent podcast I mentioned one of the biggest shifts in markets:

Investor patience has collapsed.

This chart shows it clearly that the average holding period has gone from 7 years to less than 1.

What changed?

• Always-on access to markets

• Meme stock cycles turning— Sean D. Emory (@_SeanDavid)

8:19 PM • Jul 27, 2025

GS: We raise our 12m MSCI China target from 85 to 90

— Mike Zaccardi, CFA, CMT 🍖 (@MikeZaccardi)

10:13 PM • Jul 27, 2025

Please be sure to follow us on X.

If you like what we're doing, please forward us to a friend. If you're not already subscribed, join our growing family of free subscribers.

Reply